As the Q4 earnings season comes to a close, it’s time to take stock of this quarter’s best and worst performers in the vertical software industry, including Upstart (NASDAQ:UPST) and its peers.

Software is eating the world, and while a large number of solutions such as project management or video conferencing software can be useful to a wide array of industries, some have very specific needs. As a result, vertical software, which addresses industry-specific workflows, is growing and fueled by the pressures to improve productivity, whether it be for a life sciences, education, or banking company.

The 14 vertical software stocks we track reported a satisfactory Q4. As a group, revenues beat analysts’ consensus estimates by 3.3% while next quarter’s revenue guidance was in line.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 17.1% since the latest earnings results.

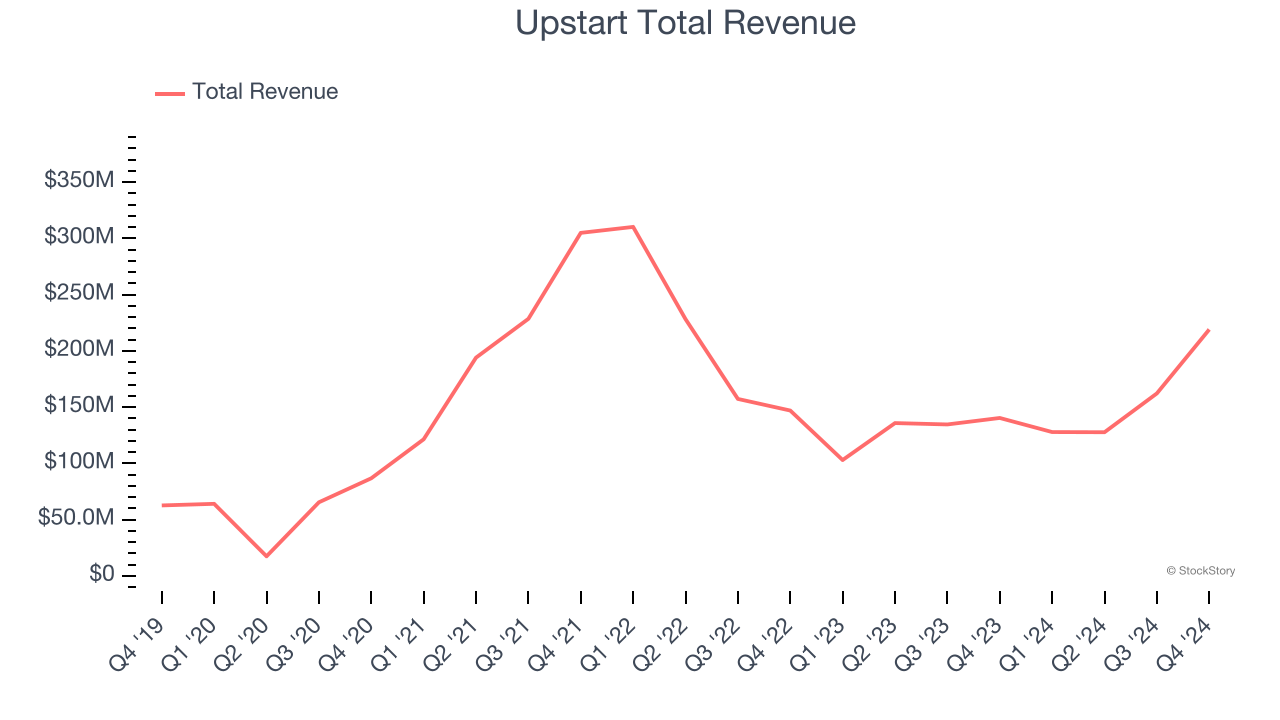

Best Q4: Upstart (NASDAQ:UPST)

Founded by the former head of Google's enterprise business, Upstart (NASDAQ:UPST) is an AI-powered lending platform facilitating loans for banks and consumers.

Upstart reported revenues of $219 million, up 56.1% year on year. This print exceeded analysts’ expectations by 20.1%. Overall, it was an exceptional quarter for the company with EBITDA guidance for next quarter exceeding analysts’ expectations.

“In Q4 of 2024, our business grew dramatically across all product categories, delivered Adjusted EBITDA at levels not seen since the first quarter of 2022, and came within a whisker of returning to GAAP profitability,” said Dave Girouard, co-founder and CEO of Upstart.

Upstart scored the biggest analyst estimates beat, fastest revenue growth, and highest full-year guidance raise of the whole group. Investor expectations, however, were likely higher than Wall Street’s published projections, leaving some wishing for even better results (analysts’ consensus estimates are those published by big banks and advisory firms, not the investors who make buy and sell decisions). The stock is down 38.8% since reporting and currently trades at $41.20.

Is now the time to buy Upstart? Access our full analysis of the earnings results here, it’s free.

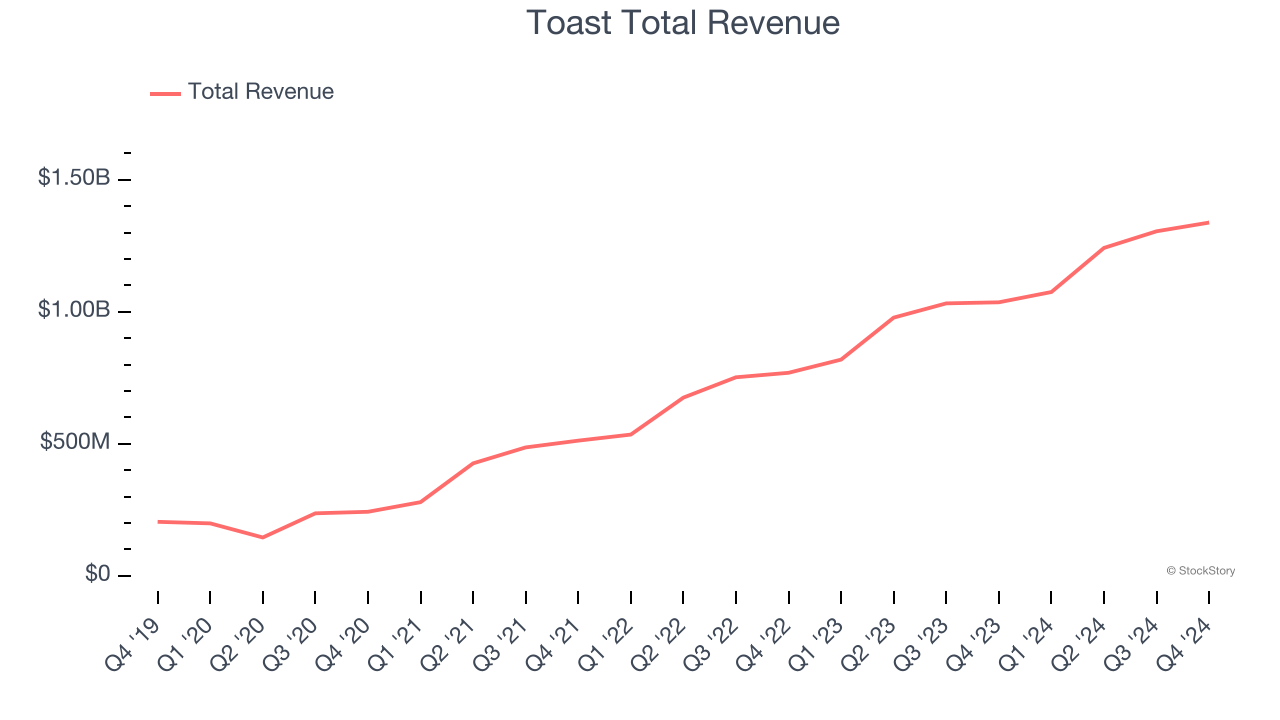

Toast (NYSE:TOST)

Founded by three MIT engineers at a local Cambridge bar, Toast (NYSE:TOST) provides integrated point-of-sale (POS) hardware, software, and payments solutions for restaurants.

Toast reported revenues of $1.34 billion, up 29.2% year on year, outperforming analysts’ expectations by 1.7%. The business had a very strong quarter with EBITDA guidance for next quarter exceeding analysts’ expectations.

The stock is down 15.1% since reporting. It currently trades at $33.96.

Is now the time to buy Toast? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: PTC (NASDAQ:PTC)

Used to design the Airbus A380 and Boeing 787 Dreamliner commercial airplanes, PTC’s (NASDAQ:PTC) software-as-service platform helps engineers and designers create and test products before manufacturing.

PTC reported revenues of $565.1 million, up 2.7% year on year, exceeding analysts’ expectations by 1.9%. Still, it was a softer quarter as it posted full-year EPS guidance missing analysts’ expectations.

As expected, the stock is down 23.3% since the results and currently trades at $145.41.

Read our full analysis of PTC’s results here.

Doximity (NYSE:DOCS)

Founded in 2010 and named for a combination of “docs” and “proximity”, Doximity (NYSE: DOCS) is the leading social network for U.S. medical professionals.

Doximity reported revenues of $168.6 million, up 24.6% year on year. This print surpassed analysts’ expectations by 9.6%. Overall, it was a very strong quarter as it also produced EBITDA guidance for next quarter exceeding analysts’ expectations.

The stock is down 6.2% since reporting and currently trades at $54.79.

Read our full, actionable report on Doximity here, it’s free.

Veeva Systems (NYSE:VEEV)

Built on top of Salesforce as one of the first vertical-focused cloud platforms, Veeva (NYSE:VEEV) provides data and customer relationship management (CRM) software for organizations in the life sciences industry.

Veeva Systems reported revenues of $720.9 million, up 14.3% year on year. This number topped analysts’ expectations by 3.1%. It was a strong quarter as it also logged a solid beat of analysts’ billings estimates and an impressive beat of analysts’ EBITDA estimates.

The stock is down 1.6% since reporting and currently trades at $216.50.

Read our full, actionable report on Veeva Systems here, it’s free.

Market Update

Thanks to the Fed’s rate hikes in 2022 and 2023, inflation has been on a steady path downward, easing back toward that 2% sweet spot. Fortunately (miraculously to some), all this tightening didn’t send the economy tumbling into a recession, so here we are, cautiously celebrating a soft landing. The cherry on top? Recent rate cuts (half a point in September 2024, a quarter in November) have propped up markets, especially after Trump’s November win lit a fire under major indices and sent them to all-time highs. However, there’s still plenty to ponder — tariffs, corporate tax cuts, and what 2025 might hold for the economy.

Want to invest in winners with rock-solid fundamentals? Check out our 9 Best Market-Beating Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.