As the Q1 earnings season wraps, let’s dig into this quarter’s best and worst performers in the online marketplace industry, including LegalZoom (NASDAQ:LZ) and its peers.

Marketplaces have existed for centuries. Where once it was a main street in a small town or a mall in the suburbs, sellers benefitted from proximity to one another because they could draw customers by offering convenience and selection. Today, a myriad of online marketplaces fulfill that same role, aggregating large customer bases, which attracts commission-paying sellers, generating flywheel scale effects that feed back into further customer acquisition.

The 13 online marketplace stocks we track reported a satisfactory Q1. As a group, revenues beat analysts’ consensus estimates by 2.2% while next quarter’s revenue guidance was in line.

Thankfully, share prices of the companies have been resilient as they are up 7.2% on average since the latest earnings results.

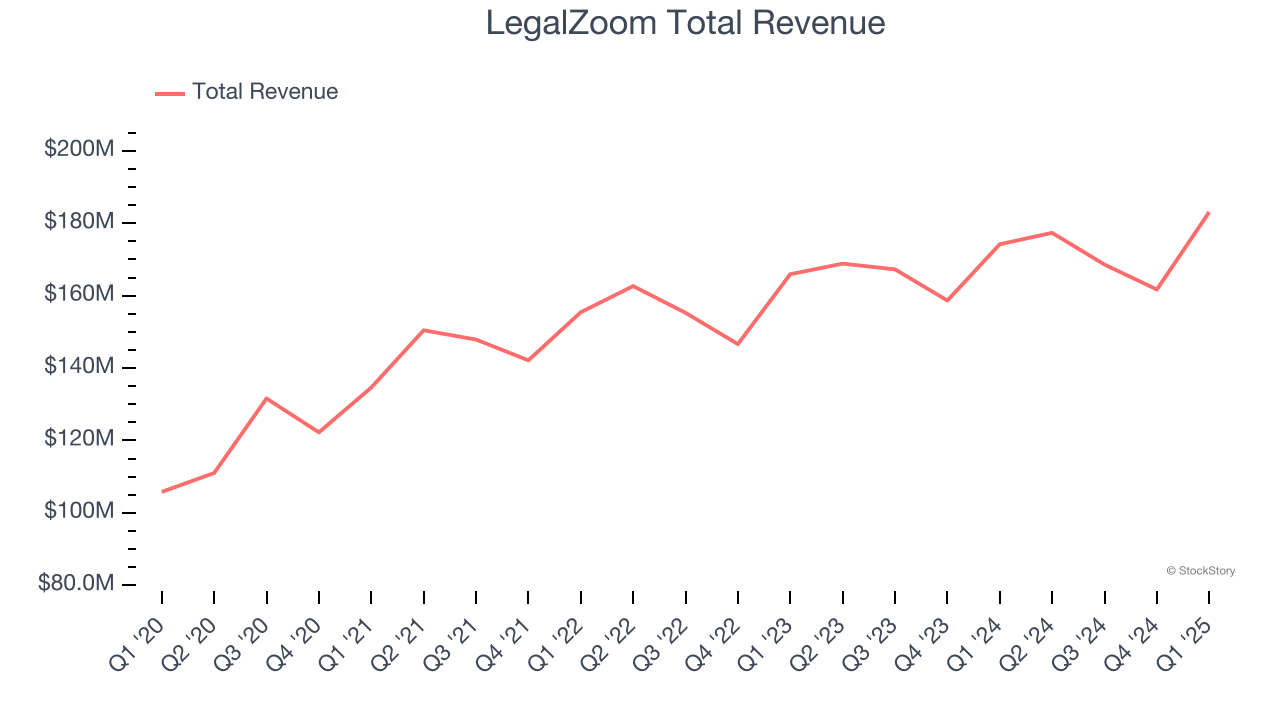

LegalZoom (NASDAQ:LZ)

Founded by famous lawyer Robert Shapiro, LegalZoom (NASDAQ:LZ) offers online legal services and documentation assistance for individuals and businesses.

LegalZoom reported revenues of $183.1 million, up 5.1% year on year. This print exceeded analysts’ expectations by 3.4%. Overall, it was a strong quarter for the company with a solid beat of analysts’ EBITDA estimates and an impressive beat of analysts’ number of subscription units estimates.

“Our first quarter results reflect accelerating subscription growth and solid progress towards our goal of double-digit subscription revenue growth in the fourth quarter,” said Jeff Stibel, Chairman and Chief Executive Officer of LegalZoom.

Interestingly, the stock is up 21.7% since reporting and currently trades at $8.84.

Is now the time to buy LegalZoom? Access our full analysis of the earnings results here, it’s free.

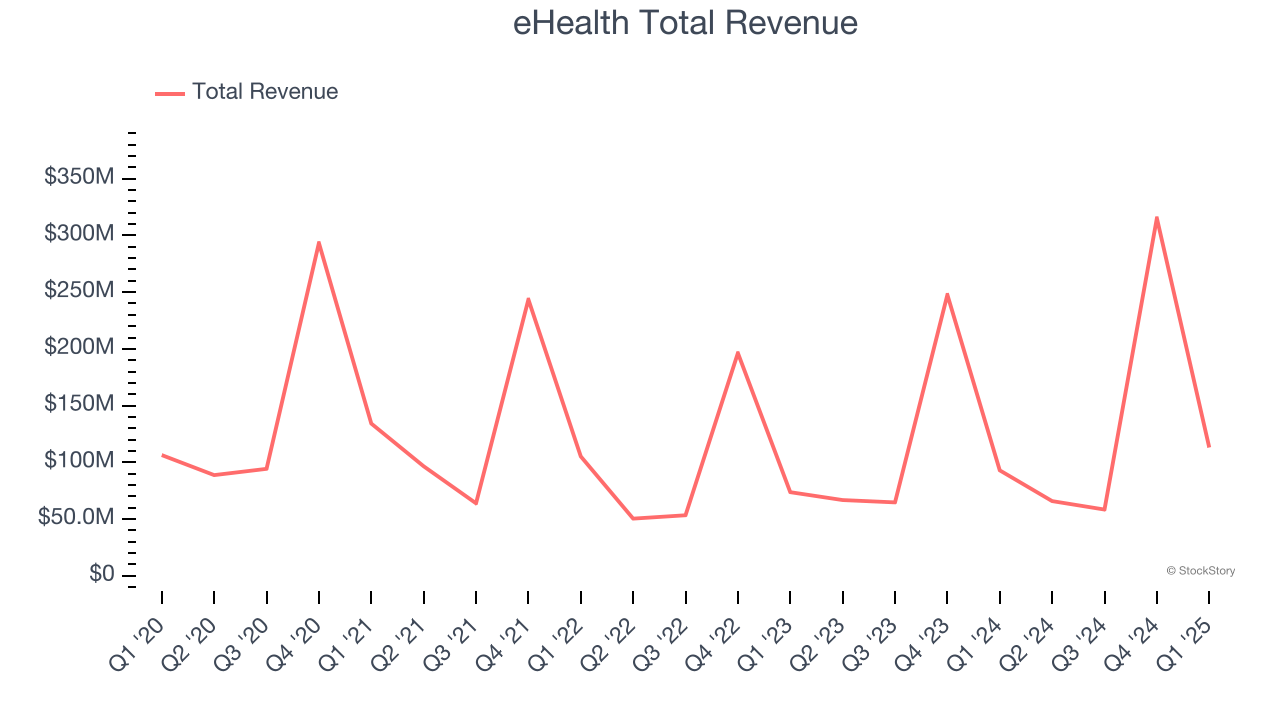

Best Q1: eHealth (NASDAQ:EHTH)

Aiming to address a high-stakes and often confusing decision, eHealth (NASDAQ:EHTH) guides consumers through health insurance enrollment and related topics.

eHealth reported revenues of $113.1 million, up 21.7% year on year, outperforming analysts’ expectations by 13.4%. The business had an exceptional quarter with a solid beat of analysts’ EBITDA estimates.

eHealth delivered the biggest analyst estimates beat among its peers. On a dimmer note, the company reported 1.16 million users, down 1.8% year on year. Although it had a fine quarter compared its peers, the market seems unhappy with the results as the stock is down 18.3% since reporting. It currently trades at $3.82.

Is now the time to buy eHealth? Access our full analysis of the earnings results here, it’s free.

Weakest Q1: The RealReal (NASDAQ:REAL)

Founded by consignment store aficionado Julie Wainwright, The RealReal (NASDAQ: REAL) is an online marketplace for buying and selling secondhand luxury goods.

The RealReal reported revenues of $160 million, up 11.3% year on year, in line with analysts’ expectations. It was a slower quarter as it posted full-year EBITDA guidance missing analysts’ expectations significantly and EBITDA guidance for next quarter missing analysts’ expectations significantly.

The RealReal delivered the weakest full-year guidance update in the group. The company reported 985,000 users, up 157% year on year. As expected, the stock is down 22.5% since the results and currently trades at $5.66.

Read our full analysis of The RealReal’s results here.

Sea (NYSE:SE)

Founded in 2009 and a publicly traded company since 2017, Sea (NYSE:SE) started as a gaming platform and has since expanded to offer a variety of services such as e-commerce, digital payments, and financial services across Southeast Asia.

Sea reported revenues of $4.84 billion, up 27.8% year on year. This result lagged analysts' expectations by 1.2%. Taking a step back, it was still a strong quarter as it recorded an impressive beat of analysts’ EBITDA estimates and a solid beat of analysts’ number of paying users estimates.

The company reported 64.6 million users, up 32.1% year on year. The stock is up 17.1% since reporting and currently trades at $167.

Read our full, actionable report on Sea here, it’s free.

EverQuote (NASDAQ:EVER)

Aiming to simplify a once complicated process, EverQuote (NASDAQ:EVER) is an online insurance marketplace where consumers can compare and purchase various types of insurance from different providers

EverQuote reported revenues of $166.6 million, up 83% year on year. This number surpassed analysts’ expectations by 5.2%. It was an exceptional quarter as it also produced EBITDA guidance for next quarter exceeding analysts’ expectations and an impressive beat of analysts’ EBITDA estimates.

EverQuote achieved the fastest revenue growth among its peers. The stock is down 5.2% since reporting and currently trades at $24.99.

Read our full, actionable report on EverQuote here, it’s free.

Market Update

As a result of the Fed’s rate hikes in 2022 and 2023, inflation has come down from frothy levels post-pandemic. The general rise in the price of goods and services is trending towards the Fed’s 2% goal as of late, which is good news. The higher rates that fought inflation also didn't slow economic activity enough to catalyze a recession. So far, soft landing. This, combined with recent rate cuts (half a percent in September 2024 and a quarter percent in November 2024) have led to strong stock market performance in 2024. The icing on the cake for 2024 returns was Donald Trump’s victory in the U.S. Presidential Election in early November, sending major indices to all-time highs in the week following the election. Still, debates around the health of the economy and the impact of potential tariffs and corporate tax cuts remain, leaving much uncertainty around 2025.

Want to invest in winners with rock-solid fundamentals? Check out our Top 6 Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.